Understanding The Potential of Real Estate as an Investment

A retired real estate attorney, Rohan’s father urged him to utilize his monthly income largely to pay for day-to-day living needs and devote money each month to long-term financial ventures like real estate when he initially entered the real estate business while attending college decades ago.

Rohan has benefited greatly throughout the years from this wise counsel. It’s never too early or late to develop your own strategy into a thorough wealth-building plan. Such a plan can assist many people with the difficulties of providing for their children’s future educational needs and assuring a pleasant retirement.

Real estate investing requires serious planning to get started. It’s much simpler to get in touch with a stock investment firm and buy some shares of your preferred mutual fund or stock than it is to buy your first rental property. Having said that, purchasing a property is actually not that tough. You may start creating your own real estate empire with a little bit of hard work, patience, and a solid financial and real estate investing strategy.

We at Gupta & Sen, provide you with some facts in this article that can assist you in determining whether you possess the necessary skills to successfully invest in real estate and generate income.

Understanding the Income and Wealth-Generating Potential of Real estate

The top advantages of real estate investing are highlighted in the list below:

Tax-deferred value compounding: When you invest in real estate, the value of your properties grows tax-deferred throughout the years that you possess them. Before selling your home, you don’t have to pay taxes on this profit since you can roll it over into another investment property and defer paying taxes until then.

Consistent cash flow: If you own real estate that you rent out, rent payments will be made each month. Larger multi-unit complexes, in particular, may include some additional sources, including coin-operated washers and dryers.

Reduced income tax bills: Depreciation is an item that can be claimed for income tax purposes but isn’t really an out-of-pocket expense. You can boost your cash flow from a property by using depreciation to lower your current income tax burden.

Rate of increase of rental income vs total expenses: As you raise your rental rates more quickly than your property‘s total expenses, over time, your operational profit, which is subject to ordinary income tax, should increase. What comes next is a straightforward illustration of how even small rental increases eventually translate into bigger operating profits and sound returns on investment.

Example

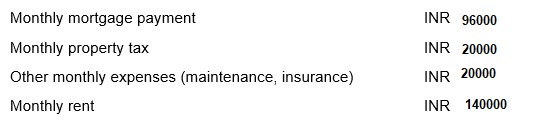

Let’s say you’re looking to buy a single-family home that you intend to rent out, and in the neighborhood, you consider to be a good investment, single-family homes are selling for around ₹ 2,00,00,000. (Note: Although housing costs range greatly depending on location, the example below should help you get a general idea of how costs and income fluctuate over time for a rental property.) You plan to pay a 20 percent down payment and borrow the remaining ₹ 1,60,00,000 using a 30-year fixed-rate mortgage at a 6 percent interest rate. Details are as follows:

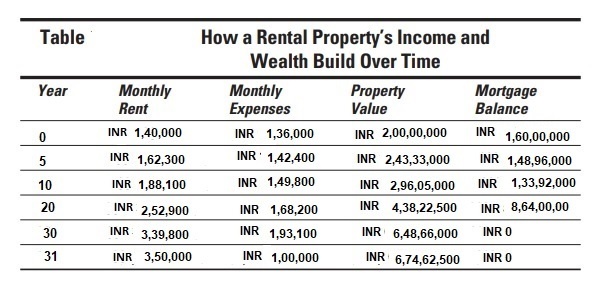

Table below displays the evolution of your investment over time. We assume that your rent and expenses (aside from your mortgage payment, which is set) will increase by 3% yearly and that the value of your home would increase by a conservative 4% yearly. (In this example, we’ll ignore depreciation to keep things simple. The calculated returns would have been improved if we had taken into account the benefit of depreciation.)

Now, see what happens over time. The monthly rent and the monthly expenses are roughly identical when you first purchase the property. By year five, there is an ₹ 20,000 monthly surplus between income and costs. Think about why your largest monthly expense, the mortgage payment, stays the same. Because of this, even while we assume that rent increases by just 3% annually — the same rate of growth we predict for your non-mortgage expenses — the compounding effect of rental inflation starts to result in an ever-increasing cash flow for you, the property owner. Even though a monthly cash flow of ₹ 2,000 may not seem like much, it comes from an initial investment of ₹ 40,00,000, generating a yearly income of ₹ 2,40,000.

As a result, by the fifth year, your rental property is earning a return on your down payment of 6%. (And keep in mind that your cash flow and return are considerably bigger if you account for the tax reduction for depreciation.)

Look at the last two columns of the Table above to see what has occurred to your equity—the difference between the market value and mortgage — by year five in addition to the monthly cash flow from the amount that the rent exceeds the property‘s expenses. Your ₹4,00,00,000 in equity (the down payment) has increased to ₹ 94,37,000 with merely a 4% annual growth in market value (₹2,43,33,000 – ₹ 1,48,96000).

By years 10 and 20, you will notice significant growth in your property’s equity as well as further increases in your monthly cash flow. You become the proud owner of a mortgage-free property worth more than quadruple what you purchased for it by year 30 and the property is generating more than ₹ 1,40,000 per month in cash flow.

Examine what happens to your monthly expenses (huge drop) and, consequently, your cash flow in years 31 and beyond when you pay off your mortgage in year 30. (big increase).

Knowing the Risks Associated with Real estate Investing

Despite its promise, real estate investing isn’t always profitable or suitable for everyone.

The following are the main disadvantages to real estate investing:

Little home runs: Your expected real estate profits won’t come close to the home runs that the most successful business people score.

Obstacles to initial operating profit: In the early stages of owning rental property, your monthly operating profit can be negligible or nonexistent unless you put down a sizable down payment.

Ups & Downs: You won’t always see an 8 to 10 percent return on your investment. Real estate ownership is not the same as owning a printing press or a successful startup, despite the possibility of substantial earnings.

Relatively high transaction costs: If you acquire a property and decide to sell it after a year or two, you might discover that even though its value has increased, the high transaction costs have eliminated most (if not all) of your profit.

Tax repercussions: Last but not least, the federal and state governments are eager to take a cut of whatever profits you generate from your real estate investment.

Comparing Other Investments to Real estate

You must have thought about or heard about a wide range of investments throughout the years. We compare and contrast real estate’s characteristics with those of other wealth-building investments like stocks and small businesses in order to help you appreciate and comprehend the special qualities of real estate. That is what we mean when we say that leverage causes the investment returns from real estate to be multiplied.

Returns

Clearly, the healthy total returns (which include ongoing profits and the value of the property) are a key factor in why so many people choose to invest in real estate. Real estate, like stocks and small businesses, is an ownership investment that produces strong long-term returns. That is to say, real estate is an asset with the potential to generate revenue and profits.

Risk

Real estate values don’t always increase; just look at the fall that took place in the majority of the United States in the late 2000s. Despite this, market values for real estate typically experience less fluctuation than stock prices.

Liquidity

One of the drawbacks of real estate is its lack of liquidity, which refers to how simple and inexpensive it is to sell an investment and withdraw your money. Real estate is relatively illiquid: You can’t sell a piece of property as quickly as you can pull out your ATM card and withdraw money from your bank account, or as quickly as you can sell a stock over the phone or with a mouse click on your computer.

Criteria for capital

The bulk of high-quality real estate investments demand far larger investments, typically on the scale of tens of thousands of dollars, but you may get started with traditional investments like stocks and mutual funds with as little as a few hundred or thousand dollars.

Diversification value

An advantage of holding investment real estate is that its value doesn’t necessarily move in tandem with other investments, such as stocks or small-business investments that you hold

Possibilities for value addition

Even though you could not be very knowledgeable about stock market investing, you might have some fantastic suggestions for how to enhance a property‘s value.

Tax benefits

Tax benefits for investing in real estate are numerous. The tax implications of investment property are contrasted with those of other investments here.

Deductible costs (including depreciation)

Property ownership is very similar to running your own small business. You report your earnings and outgoings on a tax return each year.

For the time being, we want to remind you to keep thorough records of the costs associated with buying and maintaining rental property.

Rollovers of rental property gains without taxes

You must pay taxes on your earnings when you sell an investment in a mutual fund or stock that you have outside of a retirement account. On the other hand, if you roll over your gain into another like-kind investment real estate property after selling a rental property, you can avoid paying tax on your profit.

Tax deferral and installment sales

When you sell an investment property at a profit and don’t buy another rental property, you can use the complicated procedure of installment sales to postpone paying your taxes.

Special tax incentives for aged and low-income houses

You may be eligible for special tax credits if you make improvements to registered historic structures or low-income housing. The credits provide a direct tax refund for money spent on repairing and enhancing such assets.

The Bottom Line

Real estate investment is a method that may be both rewarding and profitable. Prospective real estate owners can utilize leverage to purchase a property, unlike stock and bond investors, by paying a percentage of the total cost upfront and then paying off the balance, plus interest, over time.

Real estate investors can develop a comprehensive investment program by paying a relatively modest portion of a property‘s overall value upfront, whether they use their assets to create rental income or to pass the time until the ideal selling opportunity presents itself. Real estate offers potential for profit regardless of how the market is performing overall, as with any investment.

- Why Buyers Should Work with Agents - January 17, 2026

- Definitive Guide To Buying a Second Home - October 9, 2025

- Foreclosures REOs Probate Sales And More - October 10, 2022