The Basics of Retirement Planning

The average expectancy of human life has increased dramatically over the past 100 years or so. We are all living longer lives because of improvement of medicines and medical treatment. Every human being wants to increase his / her lifespan as much as possible but a long life comes with it’s own set of problems.

Whether you an employee or self-employed, you must start planning for providing of your daily living expenses when you get old and frail and thus the means of earning a stable and regular income are reduced. Medical expenses also shoot through the roof when you get older. This is the reason why retirement planning is of utmost importance.

The Early Bird

The importance of starting early can never be over emphasized. When people are young and working in the prime of their youth, they are busy with everything and do not give any thought about retirement planning thinking it to be a future event of little consequence right now. Retirement starts to surface in the minds of most people only when they are in their late forties and early fifties. But the worrying part is that at this age, there are fewer productive years left for a person to start saving for a fair amount of retirement corpus. Even if you do have some savings they may not be enough or it may even be negative because you may still be in the process of paying off housing or other your kid’s educational loans. Retirement planning at this stage can become an uphill task. But all is not lost. Even if there are a few years left for retirement, it is not an impossible task. But as with everything else in life, the earlier you start the better placed you are at the later stages of your life.

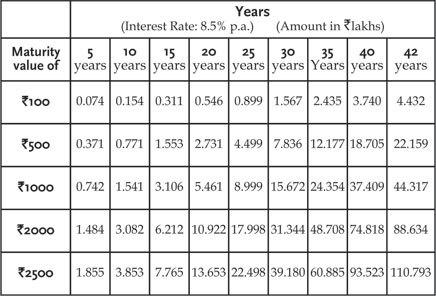

Retirement planning is best started the day you start earning a steady income. Starting this process early in life helps you harness the power of compound interest. The power of compounding is always effective over long periods of time. If you make an investment of Rs. 2500 for 4 years or Rs. 3000 for 38 years you may retire a crorepati! Have a look at the below table. It shows the maturity value of monthly savings of a fixed amount every month for a given number of years. For values that are different from these, multiply the maturity value amount of Rs. 100 pro rata.

The assumed interest rate assumed is 8.5 which is not a very hard-to-achieve figure. This is the current rate that is offered by Employee Provident Funds. The table given is for 42 years because minimum and maximum ages for employment in India is 18 and 60 years respectively. When you factor in retirement benefits and other savings that accumulate over and above your earning career, you may well become a double crorepati!

Self employed professionals can use the Recurring Deposits method to save for their retirement. Accounts that are opened under the National Pension System are also suitable for saving a fixed amount every month for getting retirement benefits.

Retirement Planning Myths

There are some myths that many people harbour and which stops them from creating a good retirement nest when the time is right. The first myth is that young people should not begin at a young age. But the reality is that the more years that are left for you to retire, the more your money gets to grow. It’s a simple but effective funda. Start saving early. And if you haven’t already start now!

The other myth lies at the opposite end of the spectrum. Then there are those who believe wrongly that retirement planning is for those who are just approaching retirement. This is obviously not true. Anyone sensible will tell you that the when your mental and physical frailties are failing you cannot draw up much of a retirement plan!

A third myth revolves around the fact that a lot of people think that it is pointless to plan for one’s retirement when you can only expect to live a few years only! Actually nothing can be farther from the truth. In the modern world, we are living longer and with increased longevity, the risk of living well into one’s 80’s and 90’s is not far fetched. We all must insure ourselves against the risk of living too long by creating an adequate retirement fund.

Retirement Planning Process

The Retirement planning process is all about figuring out the corpus that you require to generate adequate income for post-retirement. You can create a retirement plan by following the steps below:

Step 1 – Estimate the Time Plan

Decide on the number of years post retirement that you want to plan for. No one can predict how many years one will live for! A period of 30 years post retirement is a good time frame.

Step 2 – Estimate Future Monthly Expenses

This is the most crucial step. You must assess your standard of life and draw up projected monthly expenses to find out the corpus of funds that you need. You can then accordingly figure out how much you need to save.

Tips – Figure out living expenses for you and your dependents. Spends on food items like sugar, oil etc., eating out, entertainment will be lower while medical costs will be higher. Commuting expenses will be less whereas rent and maintenance costs will have to be borne. Allow for funds for traveling if you plan on taking pilgrimages, vacations or simply visiting your children and other relatives.

Step 3 – Adjust for Inflation

Convert monthly expenses to annual expenditure (multiply by 12) and adjust the final figure for inflation. What must be the rate of inflation that you must assume for this purpose? At present, the rate of inflation hovers around 9 % but you cannot go by this rate. Inflation rate must be calculated as per the CPI (Consumer price index) which may or may not impact your purchasing power to the full extent of the published rate. You must assume a rate lower than CPI-based inflation rate because CPI is based on prices of a large number of items many of which you may not consume. Like for example, vegetarians don’t consume fish, meat, poultry and eggs and non-vegetarians spend less on pluses and veggies. A weightage of 37 % is given to food but retirees do not spend that much on food and will eventually consume lesser items such as sugar and fat due to medical conditions like diabetes and heart disease. Also about 23 % weightage is given to housing cost (rent) which you may not have to consider because by the time you retire you are likely to own a house.

Also remember that inflation rates are cyclical and keep rising and falling over a long period. Inflation rates may not continue to be high throughout the post-retirement phase. Remember a few years ago inflation was only about 2 – 3 %.

Therefore I would suggest that you use a pragmatic and more realistic inflation rate that actually affects your purchasing power in the future – say around 5 – 6 %. The yearly expenses that you would now require can be adjusted for inflation by multiplying the figure with the future value of money i.e. (1 + i) to the power of n where i is the rate of inflation and n is the number of years from the present moment.

For instance, if A estimates his yearly expenses after retirement 5 years hence to be 2,00,000, then assuming an inflation rate of 6% p.a., he would require 2,00,000 × (1+0.06)⁵ = 2,00,000 × 1.33823 = 2,67,645 in order to have the same purchasing power as he gets now with 2,00,000. The value of (1+i)n can be computed with a simple calculator by (i) adding inflation rate to 100 (ii) dividing the result by 100 and then pressing the multiply button which will show results for the first year (iii) then pressing the = button for (n–1) times e.g. if n is 10 years, press = button nine times. The result will be the desired value.

Securing a regular source of income in old age is vital. You may have around 35 to 40 years of productive working life and you must create sufficient funds during this period to sustain you in your later years.

Do not miss a single article!

Submit your email id to get new articles directly into your email inbox!

- How to Cancel a Contract - May 15, 2026

- How to Prepare an Offer Agreement - May 9, 2026

- Exploring Goa in 2 Days and 7 Days - May 6, 2026